Milk prices are rising across India once again. From Punjab to Odisha and Kerala, state dairy federations have begun increasing procurement and retail prices after a prolonged period of relative stability. In Punjab, Verka has raised procurement prices significantly by Rs 20 per kg fat . OMFED has followed with a ₹1 per litre increase, while Milma has revised prices after nearly three years. Similar pressures are visible across Rajasthan, Uttar Pradesh, Karnataka , Madhya Pradesh and Andhra Pradesh.

At one level, these are routine market adjustments. But taken together, they point to something deeper. This is not a typical inflation cycle. It is a correction that has been building for years.

The immediate trigger lies in rising input costs. Over the past 18–24 months, feed prices have increased by 30–40% in many regions. Fodder availability has tightened due to erratic weather, while labour, fuel and energy costs have steadily risen. Climate stress, particularly heat waves, has further reduced milk yields during peak months, in some cases by 10–15%. The economics of dairy farming has changed, even if prices did not—until now.

For a long time, India’s dairy system functioned on a delicate balance: keep milk affordable for consumers while absorbing cost pressures within the system. Procurement prices often lagged behind rising costs, leaving farmers to carry the burden. That gap did not disappear—it accumulated. What we are witnessing today is a delayed adjustment, as institutions begin to recognise that farmer viability cannot be postponed indefinitely.

This raises a more fundamental question: what has been happening to farmer incomes during this period?

Why don’t we compute farmers income on regular basis ?

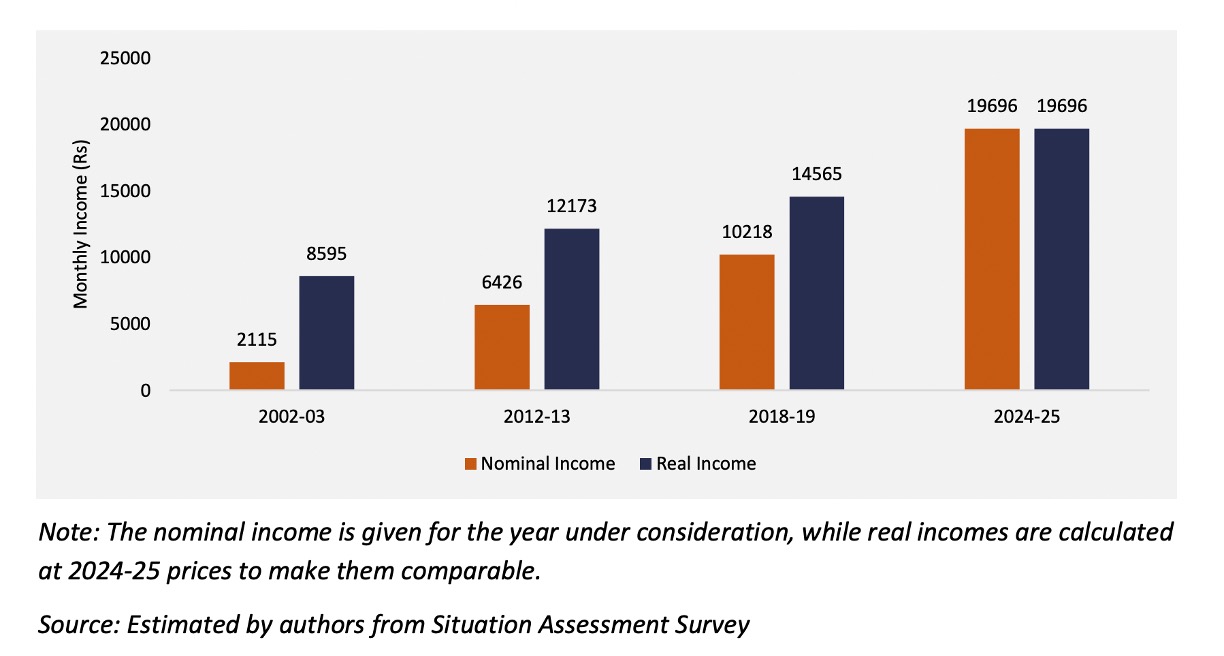

The last official nationwide estimate comes from the Situation Assessment Survey (2018–19), which placed average agricultural household income at ₹10,218 per month. More recent projections, including those by the Indian Council for Research on International Economic Relations, suggest this may have risen to around ₹19,000–20,000 by 2024–25. On paper, this appears to be a significant gain.

Average Income of Agricultural Households in India (INR)

But this is nominal growth. When adjusted for inflation and rising input costs, the picture changes. Feed, fodder, labour and energy costs have all risen sharply, eroding much of the apparent income increase. Even ICRIER acknowledges that current income levels remain low and insufficient to drive strong rural demand.

In other words, farmer incomes have increased on paper, but not proportionately in real terms.

Within this broader context, dairy plays a critical role. Households with livestock are estimated to earn over 80% higher incomes than those without, and dairy provides regular, cash-based earnings unlike seasonal crops. It supports more than 75 million rural households and remains one of the most stable components of farm income.

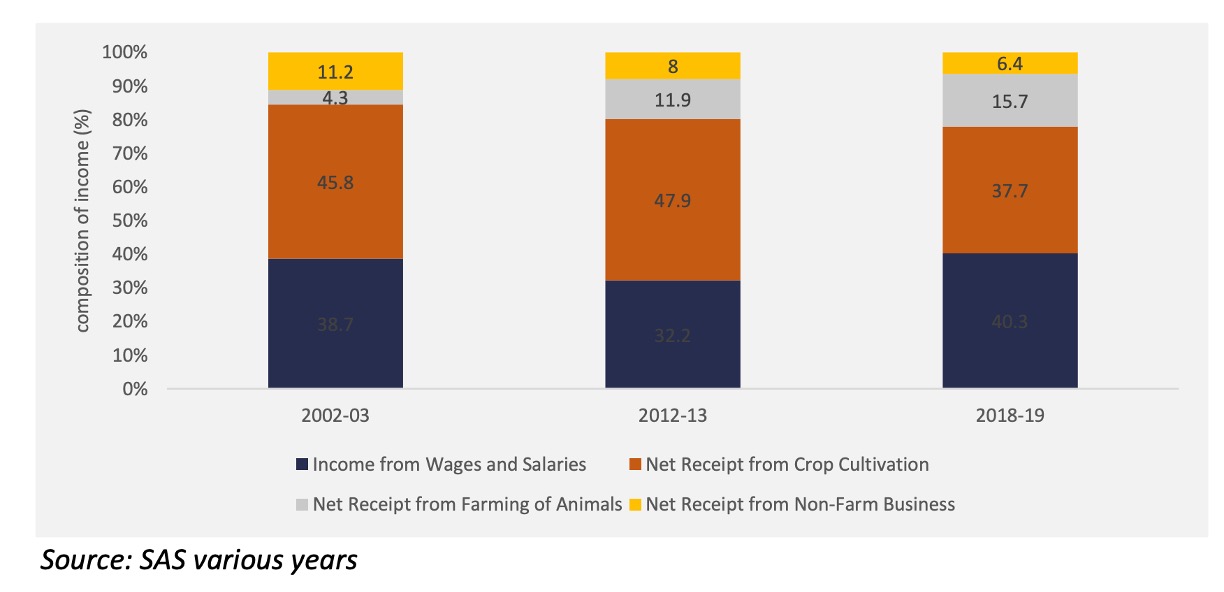

Composition of Income of Agricultural Households, 2002-03 to 2018-19

Data from successive Situation Assessment Surveys shows a clear structural shift in farmer incomes. The share of income from crop cultivation has declined from nearly 48% in 2012–13 to about 38% in 2018–19. In contrast, income from livestock—primarily dairy—has increased nearly fourfold from just over 4% in 2002–03 to close to 16% in 2018–19. This makes dairy one of the fastest-growing components of farm income. Yet, this rising dependence is not matched by commensurate income growth, as rising input costs continue to compress margins.

There is little clarity on cost of production, regional margins, or how much farmers actually earn after accounting for rising input costs. Livestock as the most reliable source of rural income remains one of the least measured.

This gap matters. Because without understanding real income dynamics, policy risks misreading price signals. The current rise in milk prices is not an aberration—it is a necessary correction. Farmers are not earning more today; they are beginning to recover what they should have earned earlier.

The way forward

The way forward must go beyond periodic price hikes. Farmers need productivity-led gains through better feeding practices, improved genetics and scientific herd management. Processors must move beyond liquid milk to value-added products that can sustain higher procurement prices. Consumers, too, need transparent communication on why prices are rising. And policymakers must enable rather than suppress—through investments in fodder systems, climate resilience and decentralised infrastructure.

Most importantly, India needs to start measuring what it seeks to improve. An updated, inflation-adjusted assessment of farmer incomes—particularly in dairy—is no longer optional.

Because the future of India’s dairy sector will not be defined by how much milk it produces, but by how fairly that value is shared.

For years, India’s dairy success was measured by how much milk it could produce. The next phase will be defined by a different question—whether that milk can be produced sustainably, with farmers earning fairly and the system remaining resilient.

Because in dairy, affordable milk can be engineered for a while. Sustainable milk, however, must be built.

Source : Blog by Kuldeep Sharma Chief Editor Dairynews7x7.com May 2nd 2026