The latest economic assessments emerging from SBI Ecowrap during May 2026 may appear, at first glance, to be another routine macroeconomic outlook discussing GDP moderation, crude oil risks, currency pressure and labour income slowdown. However, for those who understand the structural realities of India’s dairy economy, these reports carry a far deeper warning. They indicate that the Indian dairy sector may be approaching one of the most difficult cost-and-consumption cycles witnessed since economic liberalisation.

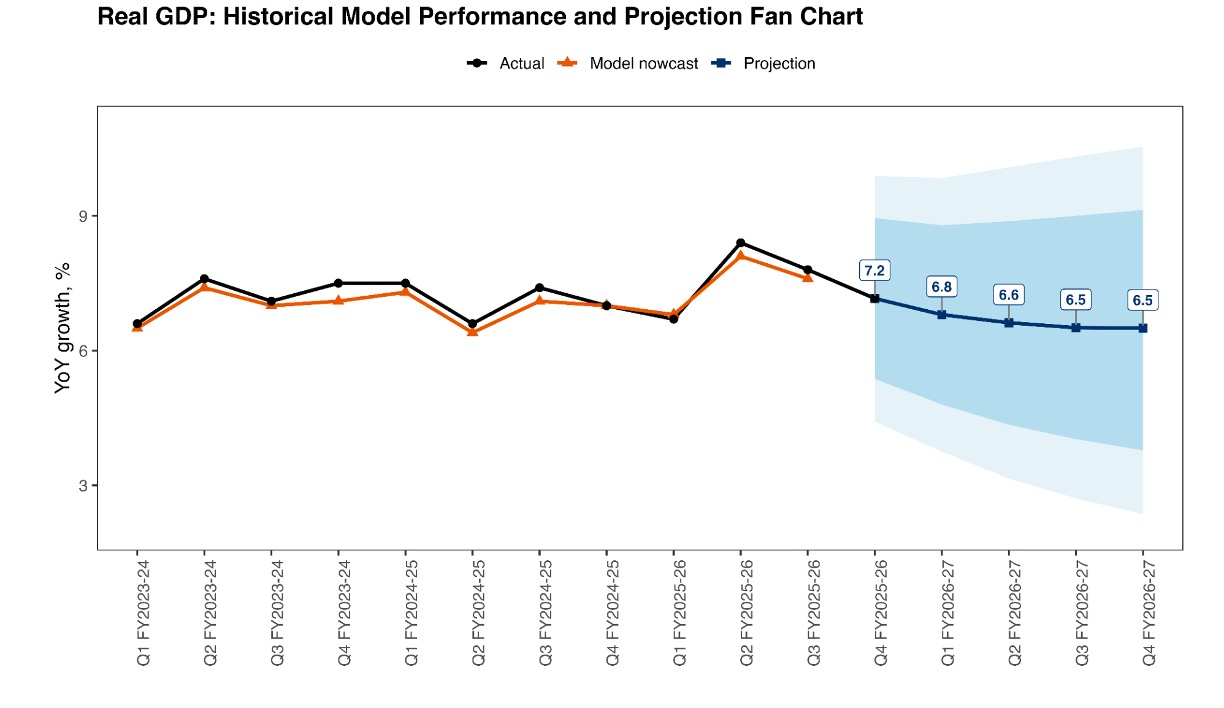

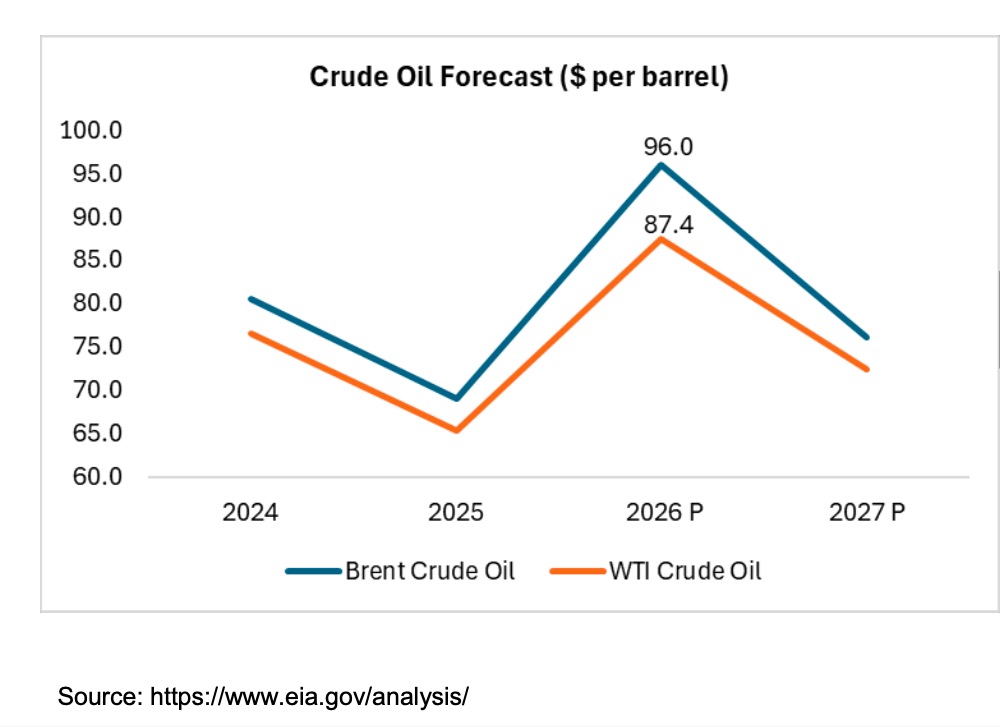

SBI Research has projected India’s GDP growth for FY27 at nearly 6.6%, substantially lower than the stronger momentum seen during FY26. The concern is not merely about a reduction in growth numbers. The larger issue lies in the combination of rising geopolitical uncertainty, elevated crude oil prices, imported inflation, weakening labour income growth, currency volatility and pressure on domestic consumption. At the same time, global agencies have warned that sustained crude oil prices at elevated levels could shave off a significant portion of India’s economic growth while simultaneously hurting corporate profitability across sectors. For India, which imports nearly 85 percent of its crude oil requirement, this is not a theoretical risk. It is a direct economic transmission channel that can influence almost every component of the dairy value chain.

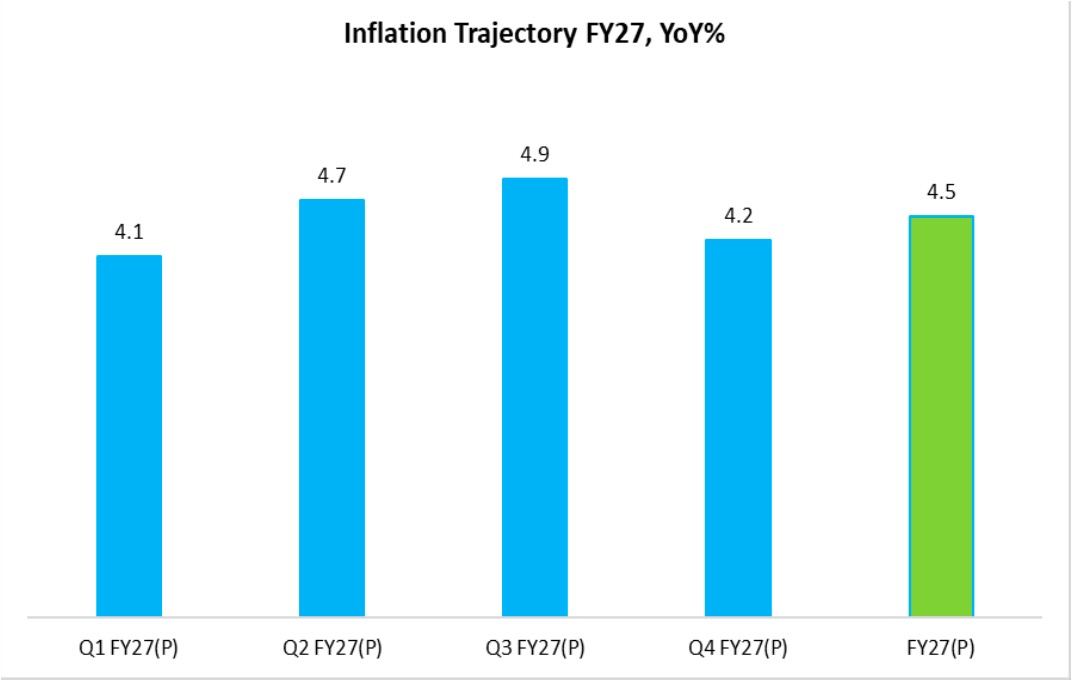

Source : SBI report Outlook FY 27

The Indian dairy industry is perhaps one of the most macro-economically sensitive sectors within the food economy. Milk must be collected twice every day from millions of farmers, chilled immediately, transported under temperature-controlled systems, processed through energy-intensive operations, packed in petroleum-linked materials and distributed daily across vast retail networks. Very few industries operate under such a continuous and unforgiving supply chain structure. Unlike many manufacturing sectors, dairies cannot stop procurement because raw material continues arriving every morning. As a result, the industry absorbs inflationary shocks in real time.

Farm level stress

The first signs of stress are likely to emerge at the farm level. Feed economics in India have already remained under pressure due to volatility in maize, oilcakes and protein supplements. If crude oil prices remain elevated and the rupee weakens further against the dollar, imported feed additives, mineral mixtures, bypass fats, amino acids, veterinary supplements and specialty nutrition inputs will become significantly more expensive. Feed already contributes nearly 65 to 70 percent of milk production cost in commercial dairy systems. Even a moderate increase of 8 to 12 percent in feed cost can sharply affect farmer profitability, particularly among smallholders operating with limited financial resilience.

The larger concern, however, is not simply rising input costs but the behavioural response that follows. When dairy farmers face economic pressure, the first adjustment often comes through reduction in concentrate feeding. This gradually lowers milk yield, weakens fat and SNF percentages, affects animal health and reduces lactation efficiency. India may therefore witness a dangerous paradox during FY27 where milk procurement prices continue rising while overall productivity growth slows down. Such a situation can severely compress margins for organised dairies because long-term profitability in the dairy industry depends more on productivity gains than on simple expansion of procurement volumes.

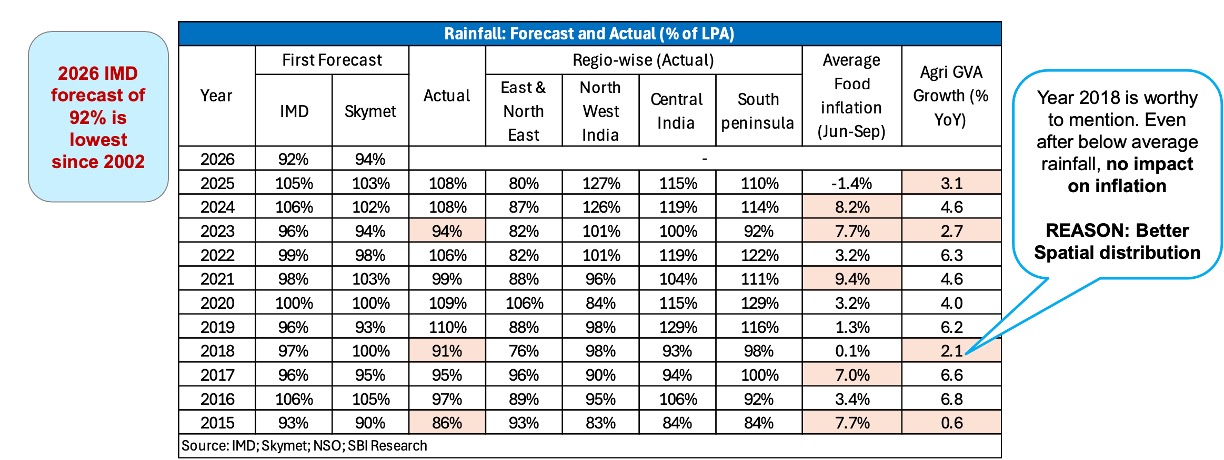

Fodder economics could emerge as another major stress point during the coming quarters. Rising diesel prices directly affect irrigation cost, fodder harvesting, silage transportation, baling operations and rural logistics. If monsoon variability appears during FY27 (as shown above ), green fodder inflation could intensify sharply, especially during the second and third quarters of the fiscal year. Historically, whenever fuel inflation combines with fodder shortages, milk production growth weakens after a lag of one or two quarters. The sector may therefore witness rising dry fodder prices, regional feed shortages, increased dependence on commercial cattle feed and even distress sale of low-yielding animals in vulnerable regions. This could alter India’s milk growth trajectory more seriously than currently anticipated.

Macro economic factors

Another critical signal emerging from the SBI analysis relates to the slowdown in labour income growth. This point may appear disconnected from dairy at first glance, but it has deep implications for the sector. Dairy consumption in India is closely linked with rural cash flows, informal labour earnings and lower-middle-class purchasing power. When wage growth slows in construction, MSMEs and rural employment segments, discretionary dairy consumption also weakens. Liquid milk demand may remain relatively stable because milk is nutritionally and culturally embedded in Indian households, but the pressure could become visible across premium and value-added dairy categories.

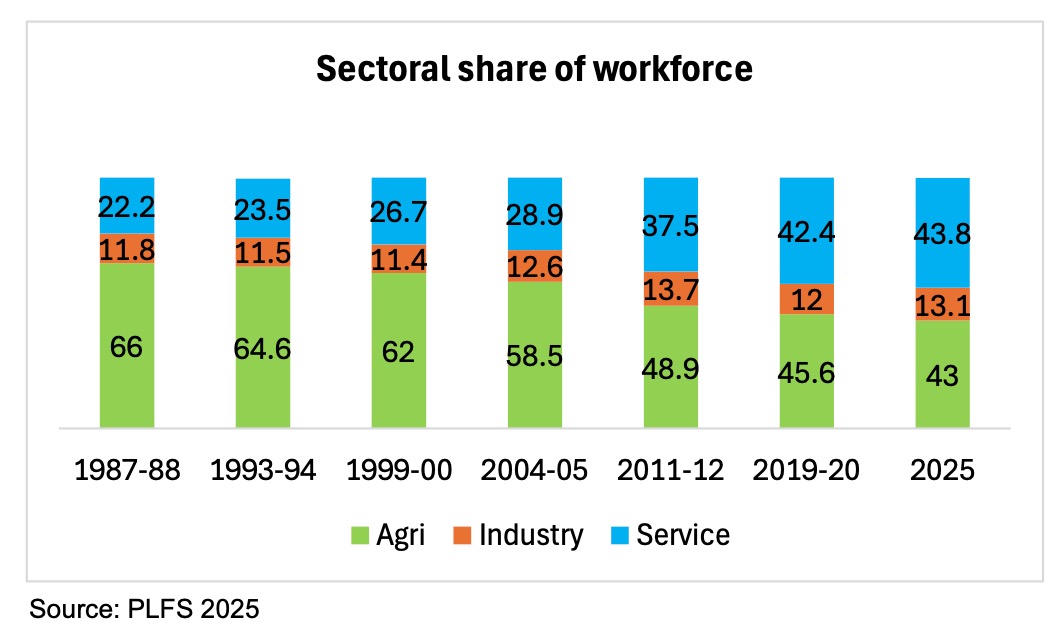

As per SBI report,

- “The share of agriculture in India’s workforce has declined from nearly 66% in 1987-88 to around 43% in 2023-24 — a reduction of almost 23 percentage points over the past 37 years. Rising rural aspirations, migration toward non-farm employment and changing socio-economic dynamics, including increasing female participation across diversified rural occupations, are steadily altering the structure of India’s agricultural labour economy. At a time when input costs are rising, farm profitability remains under pressure and the younger generation is moving away from agriculture, an uncomfortable but critical question now emerges before policymakers and industry alike — who will produce milk and food for India in the coming decades?”

India may therefore enter a temporary phase of “de-premiumisation” in dairy consumption. Consumers are unlikely to stop purchasing milk, but they may begin reducing expenditure on cheese, ice creams, probiotic beverages, premium curd, gourmet butter, dairy desserts and high-value nutritional products. Smaller stock-keeping units may gain traction as consumers attempt to manage household budgets. The organised dairy industry may discover that the next phase of demand growth will not come easily through premiumisation narratives alone.

Fuel inflation may become the single most disruptive factor across the dairy value chain. Every litre of milk in India travels through an extensive procurement network involving village collection centres, milk routes, bulk milk coolers, chilling plants, tankers and refrigerated logistics systems. Even a moderate increase in diesel prices can significantly increase milk procurement cost per litre. Remote milk sheds may become economically unviable, while low-density procurement geographies could lose attractiveness for private dairies. This may accelerate a structural shift toward cluster-based procurement systems, regional processing hubs and shorter supply chains. In many ways, FY27 could redefine how milk sourcing networks are designed in India.

Packaging Material the second largest cost after Raw material

The hidden but potentially most severe crisis may emerge from packaging economics. Packaging today constitutes one of the fastest-growing cost heads for organised dairies. The sector depends heavily on LDPE films, multilayer laminates, PET, polypropylene, plastic crates, caps, closures and aseptic packaging materials, almost all of which are linked directly or indirectly to crude oil and imported petrochemical chains. A combination of high crude prices and rupee depreciation can sharply inflate packaging costs. Flexible packaging materials may witness double-digit inflation, while imported aseptic cartons and polymer-linked materials could become substantially more expensive.

For value-added dairy businesses, this challenge becomes even more serious because packaging intensity per litre is significantly higher compared to liquid milk. In several product categories, packaging inflation may rise faster than milk inflation itself. The likely industry response may include grammage reduction, selective price hikes, smaller pack sizes, simplified packaging structures, reduction in promotional expenditure and rationalisation of product portfolios. Smaller regional dairies may suffer the most because they lack the purchasing scale and procurement leverage enjoyed by larger organised players.

Boom time for Local dairy Engineering and Value added Ingredients Eco system

The weakening rupee may also create major implications for India’s dairy infrastructure expansion plans. The country continues to import significant dairy processing technologies from Europe and North America, including membrane systems, spray dryers, PLC automation, cheese processing technologies, instrumentation systems, homogenisers and advanced filling lines. Currency depreciation can sharply increase project costs and delay return-on-investment calculations. As a result, expansion projects may slow down during FY27, and automation investments may face postponement across several dairy businesses.

Ironically, however, this stress may simultaneously create a historic opportunity for Indian dairy engineering companies. Rising import costs could accelerate localisation of dairy technologies and strengthen domestic manufacturing capabilities in process engineering, automation systems and fabrication. India may witness stronger momentum toward indigenous dairy technology development and affordable engineering solutions not only for domestic markets but also for exports.

Source SBI Research 2026

Imported dairy ingredients may face similar inflationary pressure. Whey protein concentrates, specialty cultures, enzymes, nutraceutical ingredients, stabilisers and functional ingredients are all vulnerable to currency and freight fluctuations. Consequently, innovation in sports nutrition, functional dairy, protein beverages and clinical nutrition products may temporarily slow as companies become more cautious about product development and portfolio expansion.

Perhaps the greatest challenge for the organised dairy sector during FY27 will be simultaneous margin compression. The industry may face rising milk procurement prices, increasing fuel costs, escalating packaging expenses, higher energy tariffs, growing labour costs and elevated finance charges, all while consumer affordability weakens and pricing flexibility reduces. This creates a classic economic squeeze where costs rise faster than purchasing power. The impact may become particularly severe for ice cream businesses, cheese manufacturers, SMP-heavy processors, highly leveraged dairies and smaller regional players operating on thin margins.

Cooperatives with captive milk procurement display resilience

At the same time, certain categories of dairy businesses may display greater resilience. Strong liquid milk brands, cooperatives with dense procurement networks, companies integrating renewable energy solutions and processors operating through efficient regional supply chains may withstand the turbulence more effectively. The next phase of dairy competition may therefore be decided not by installed capacity alone but by operational efficiency, energy management, logistics optimisation and financial discipline.

The coming four quarters of FY27 may gradually unfold as a transition period for the dairy sector. The first quarter may witness the beginning of cost escalation. The second quarter could become decisive depending upon monsoon performance and fodder availability. The third quarter may bring festive demand but also severe pressure on packaging and working capital. By the fourth quarter, the industry could enter a phase of restructuring, consolidation and strategic rationalisation.

India’s dairy sector is certainly not heading toward collapse. Milk remains deeply integrated into the country’s food culture, nutrition security and rural livelihood economy. However, the industry may soon enter a defining correction cycle where efficiency becomes more important than expansion, productivity matters more than procurement volume and economic resilience becomes more valuable than aggressive scale-building.

The latest SBI Ecowrap findings should therefore not be viewed merely as another macroeconomic report. For the Indian dairy industry, they represent an early warning that the era of relatively easy growth may be ending.

The next decade may not belong to the largest dairy companies, but to those capable of controlling costs, improving productivity, optimising supply chains, managing energy exposure and adapting quickly to a far more demanding economic environment.

Source : Analysis of SBI Economic report 2026 by Kuldeep Sharma Chief editor Dairynews7x7